Was 2015 really the year of Apple Pay?

Was 2015 really the year of AppleWas 2015 really the year of Apple Pay? Pay?

According to Tim Cook, 2015 was when Apple Pay would make its mark.

That claim left an indelible impression on the minds of those with press credentials. What constitutes a device, service, company or anything else to brand a year its own?

Or was it all just more spin coming from Cupertino?

What is Apple Pay?

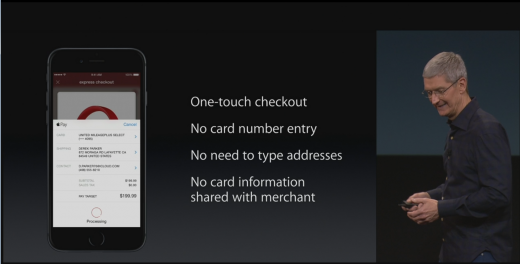

Newer iOS devices have an Near Field Communications (NFC) chip that allows the phone to wirelessly communicate with some point of sale terminals where you normally do things like swipe a credit card.

That NFC chip also transmits information between your bank and the terminal. It sends information using an encrypted key, so even if some nefarious hacker intercepted the info, they’d have no way to decode and use it.

Apple Pay requires partnerships from financial institutions; the bank issuing your card has to authorize it for Apple Pay. That’s not only because they need to make sure the transactions are initiated by you, but because Apple takes a small cut of the transaction (0.015 percent).

Biometrics also safeguard the transaction; users must confirm all purchases with the Touch ID fingerprint sensor surrounding the home button.

A business also has to have hardware capable of accepting Apple Pay. You can’t walk into any restaurant and pay with Apple Pay just yet — but it’s catching on (a full list of both banks and restaurants compatible with Apple Pay can be found on Apple’s dedicated website).

Why was 2015 supposed to be ‘the year of Apple Pay’?

In short, because Tim Cook said so.

During Apple’s first quarter conference call discussing earnings, Cook said Apple was getting “extremely positive” feedback about Apple Pay, leading him to announce 2015 as the “year of Apple Pay.”

“Point of sale suppliers tell us they are seeing unprecedented demand from merchants, and all of our partners and customers simply love this new service. With all of this momentum in the early days, we are more convinced than ever that 2015 will be the year of Apple Pay.”

The competition

On launch, Apple Pay had only a cobwebbed Google Wallet that posed a direct threat to its mobile payment initiatives. There was alsoCurrentC lurking about.

CurrentC was a mobile payment option backed by heavy-hitting retailers like WalMart, Target (which is rumored to have its own mobile payment scheme in the works) and CVS. In adopting that unreleased technology, those retailers also rebuffed the ready-and-willing Apple Pay. Unlike Apple Pay or Google Wallet, CurrentC didn’t have a technology company’s blessing (or name). It was simply an idea left on the vine too long.

Another challenger was Samsung, who snapped up a small company named Looppay and rebranded its technology as Samsung Pay. Unlike Apple Pay (or Google Wallet), Samsung Pay didn’t need a special terminal to process transactions; it works with any that can swipe a card.

Since shuttering Wallet as a forward-facing product and buying Softcard, Google has rebranded its mobile payment solution as Android Pay. Oh, and LG may also be getting into the mix.

Oddly, Apple actually gets in its own way of faster adoption for Apple Pay. A lot of boxes have to be ticked before it works: you need a newer iOS device, a debit or credit card that works with Apple Pay and a business that acceptsApple Pay (with a point-of-sale terminal that works properly).

Apple does not make Apple Pay available outside of its own hardware ecosystem, mainly because its technology demands an NFC chip do nothing more than process payments. Its own proprietary use of hardware and software makes that a possibility.

Signs of success

At launch, Apple Pay had some notable backing. Visa, Mastercard and American Express were all on board, representing about 90 percent percent of the potential credit card transactions in the US.

Apple Pay is also continuing to roll out globally. It’s now available in the UK, and most recently hit Canada (via American Express). China will have it in 2016.

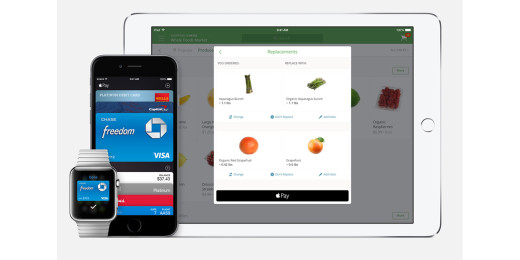

You can do anything from buy burritos to pay rent with Apple Pay. Apple was an obvious early adopter; Apple Pay is available in every Apple Store, and in the Apple Store app.

For developers, working Apple Pay into apps is as simple as plugging in an API; Apple does all the heavy lifting.

So was 2015 the year of Apple Pay?

During quarterly earnings calls, Apple CEO Tim Cook continues to say all the right things about Apple Pay being successful.

Platitudes aside, it’s hard not to consider Apple Pay to have made a significant impact in 2015. Not only did it accelerate the use of mobile payments (something Google couldn’t do with Wallet, for various reasons), but it got people talking about using their phones, tablets and watches to pay for stuff. It’s also available in apps, making it much easier to buy things on your phone before you pick them up in-store.

There is at least one app dedicated to finding Apple Pay locations, andSquare has launched an NFC card reader that focuses its marketing energy on the fact it will accept Apple Pay (it will accept any NFC-enabled mobile payments transaction).

Square may be a missing link for Apple Pay, too. It’s open to anyone; a small business or weekend fair vendor can make a living from it. You could even keep one lying around the house to let friends repay loans with credit cards if you were inclined.

While Apple does the heavy lifting of getting big retailers on board, Square will pick up the mom-and-pop shops and upstart restaurants.

But that’s future-facing commentary; what about 2015?

It’s hard to say any other mobile payments solution has had the impactApple Pay has this past year. Really, it’s hard to argue any mobile payment solution having ever been as forceful. Solutions existed before Apple Pay, and new ones are popping up all the time, but Apple’s own reigns supreme.

2015 was the year of Apple Pay, but 2016 will test its mettle — and whether or not it’s truly the dominant mobile payment solution many want it to be.